I installed NetGuard about a month ago and blocked all internet to apps, unless

they’re on a whitelist. No notifications from this particular system app (that

can’t be disabled) until recently when it started making internet connection

requests to google servers. Does anyone know when this became a thing? Edit 2: I

bought my Pixel 6 phone outright, directly from Google’s Australian store. I

have no creditors. Were the courts not enough control for creditors? Since when

are they allowed to lock you out of your purchased property without a court

order? I don’t even live in the US, so what the actual fuck? Edit 1: You can

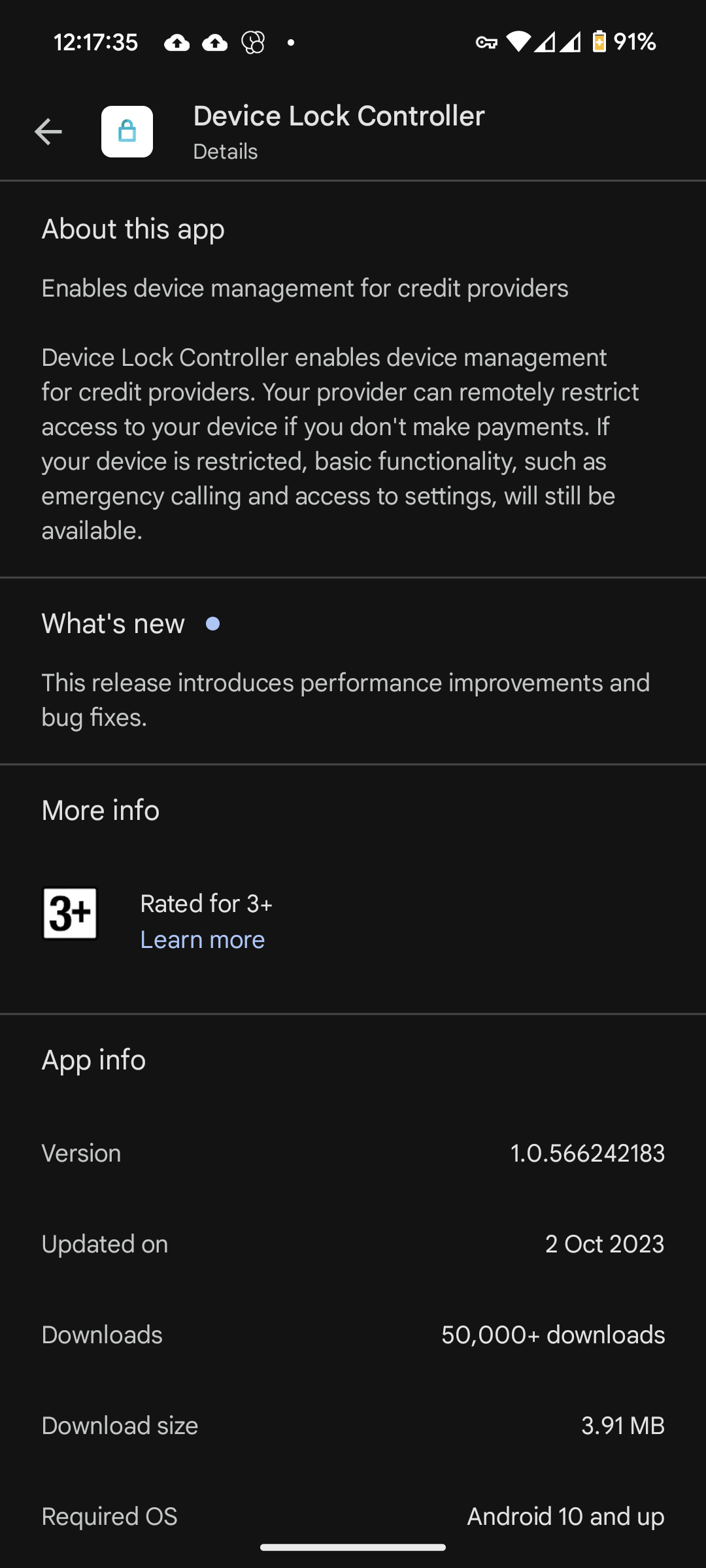

check it’s installed (stock Pixel 6 android 14) Settings > Apps > All Apps >

three dot menu, Show system > search “DeviceLockController”. I highly recommend

getting NetGuard, you can enable pro features via their website if you have the

APK for as low as 0.10€, but donate more, because it’s amazing. You can also

purchase via Google Play store.

The real problem with @Blaster_M@lemmy.world’s comment was to blame the victim. It may be sensible to blame the victim, but let’s not lose focus on the perp.

I must say Paypal shares customer data with over 600 corporations among other scummy things, so I boycott them. I also boycott eBay because the javascript required to use their website port sniffs your LAN and feeds that back to them, apart from other evils.

But most importantly, I’m not necessarily worried that I would personally get burnt by this. But just like my unwillingness to buy an Intel CPU with a management engine (or AMD’s flavor of this), I am unwilling to buy a product that was designed to work against me. I do not want to finance anti-consumer suppliers. ATM I don’t know how to check whether my version of AOS has this “feature”.

(BTW, I’m not the OP; I just linked their post here)

Sniffs your local pc to look for remote desktop and vnc ports on it. I can see this being useful in finding RAT risks, but the portscan thing is something the browser should be blocking or sandboxing.

As for PayPal, well, your cc / bank also shares lots of data.

If your threat modelling is that severe, your best bet is Tor Craigslist, a couple blokes packing heat and a briefcase of money in a place with no parking lot surveillance.

But then at that point security and safety is on you and your mates to implement.

As for PayPal, well, your cc / bank also shares lots of data.

Paypal is not a bank. Paypal is an additional MitM. Using Paypal adds another surveillance capitalist to the chain along with your bank and credit network. But indeed, the banks and credit cards are shit so I am fighting the war on cash quite hard. I’ve already been dragged into court for insisting on paying a creditor in cash. I won that case and will continue insisting on cash payments.

If your threat modelling is that severe

My threat model simply includes mass surveillance. Which is in the threat model of everyone who understands and embraces privacy. It’s worth noting that it’s not purely and infosec stance. I also object to feeding a supplier who is acting against me. The moment I detect that a supplier is working against me, I walk on ethical grounds. They have failed to earn my business. The snooping just happens to be the manner in which they are working against me.

your best bet is Tor Craigslist,

I was doing that at one time but something pushed me off. I don’t recall what… whether it was SMS verify or CAPTCHAs or phone numbers or fussy email address verifiers… something drove me off.

Most of my shopping is done at street markets. When a big parking is filled with vans and portable tables on a weekly basis, there is no surveillance. But if I need something very particular then the cash option gets threatened. E.g. I would like to have a Flipper Zero but these are never at street markets and not even on any shelves anywhere.

I have a Flipper Zero (and case and the extra components) that I’ll 99.99% likely never use. I’d love to get cash for it but I’d be asking twice what it’s worth because I like having it on ‘what if’ grounds.

But I feel you, it’s unfortunate about the state of things. The EU just banned privacy coins. US is soon coming I’m sure. They won’t allow people to legally use them after the release of a central bank coin.

Ethical consumers patronize the lesser of evils, and go without if it’s feasible given only quite shitty options. Affluenza-driven OCD consumption is the unhealthy obsession that ethical consumers manage to avoid.

I’m OOP, I bought this Pixel 6 phone outright directly from Google. This system app has no business being on my phone.

And even IF it was purchased on credit, this is such an unfair power dynamic which hurts the most vulnerable in society.

Miss a phone payment, get locked out, haha have fun trying to access your bank account (many people have a phone as their primary computing device to access banking, and further, many banks might have SMS 2FA).

I say, there is no excuse for this. There were repo methods before software locks, and we’d ought to keep it that way.

It doesn’t appear to actually be used, at least in Australia, but having the functionality built in at all should be straight up illegal in a caring society.

I don’t think any of the major (I know someone will probably come in here and tell me about some tiny provider that’s only in like 2 states that does) US carriers that do phones on secured credit, they default to unsecured credit. Maybe, they have an alternative plan for people with not so great credit, but I doubt it.

Someone in the original thread said this swindle does not apply to the US. Though I’m a bit surprised… it’s the first place where I would expect this to happen.

Don’t buy a phone on collateral credit (like from a cell provider that “gives” you a phone with service). If you must, ebay a phone and use paypal.

If you can’t afford a $1200 phone by paying for it in “cash”, you need to aim lower.

Comments from the last post indicated it made no difference to having the killswitch on their devices as per screenshots.

Still I agree, buying on credit is not a good idea.

The real problem with @Blaster_M@lemmy.world’s comment was to blame the victim. It may be sensible to blame the victim, but let’s not lose focus on the perp.

I must say Paypal shares customer data with over 600 corporations among other scummy things, so I boycott them. I also boycott eBay because the javascript required to use their website port sniffs your LAN and feeds that back to them, apart from other evils.

But most importantly, I’m not necessarily worried that I would personally get burnt by this. But just like my unwillingness to buy an Intel CPU with a management engine (or AMD’s flavor of this), I am unwilling to buy a product that was designed to work against me. I do not want to finance anti-consumer suppliers. ATM I don’t know how to check whether my version of AOS has this “feature”.

(BTW, I’m not the OP; I just linked their post here)

Sniffs your local pc to look for remote desktop and vnc ports on it. I can see this being useful in finding RAT risks, but the portscan thing is something the browser should be blocking or sandboxing.

As for PayPal, well, your cc / bank also shares lots of data.

If your threat modelling is that severe, your best bet is Tor Craigslist, a couple blokes packing heat and a briefcase of money in a place with no parking lot surveillance.

But then at that point security and safety is on you and your mates to implement.

Paypal is not a bank. Paypal is an additional MitM. Using Paypal adds another surveillance capitalist to the chain along with your bank and credit network. But indeed, the banks and credit cards are shit so I am fighting the war on cash quite hard. I’ve already been dragged into court for insisting on paying a creditor in cash. I won that case and will continue insisting on cash payments.

My threat model simply includes mass surveillance. Which is in the threat model of everyone who understands and embraces privacy. It’s worth noting that it’s not purely and infosec stance. I also object to feeding a supplier who is acting against me. The moment I detect that a supplier is working against me, I walk on ethical grounds. They have failed to earn my business. The snooping just happens to be the manner in which they are working against me.

I was doing that at one time but something pushed me off. I don’t recall what… whether it was SMS verify or CAPTCHAs or phone numbers or fussy email address verifiers… something drove me off.

Can’t help you there. Buying stuff isn’t anonymous, even brick and mortar stores have cloud surveillance cams now.

Most of my shopping is done at street markets. When a big parking is filled with vans and portable tables on a weekly basis, there is no surveillance. But if I need something very particular then the cash option gets threatened. E.g. I would like to have a Flipper Zero but these are never at street markets and not even on any shelves anywhere.

I have a Flipper Zero (and case and the extra components) that I’ll 99.99% likely never use. I’d love to get cash for it but I’d be asking twice what it’s worth because I like having it on ‘what if’ grounds.

But I feel you, it’s unfortunate about the state of things. The EU just banned privacy coins. US is soon coming I’m sure. They won’t allow people to legally use them after the release of a central bank coin.

So you just don’t buy anything? Get over yourself and your unhealthy obsessions.

Ethical consumers patronize the lesser of evils, and go without if it’s feasible given only quite shitty options. Affluenza-driven OCD consumption is the unhealthy obsession that ethical consumers manage to avoid.

I’m OOP, I bought this Pixel 6 phone outright directly from Google. This system app has no business being on my phone.

And even IF it was purchased on credit, this is such an unfair power dynamic which hurts the most vulnerable in society.

Miss a phone payment, get locked out, haha have fun trying to access your bank account (many people have a phone as their primary computing device to access banking, and further, many banks might have SMS 2FA).

I say, there is no excuse for this. There were repo methods before software locks, and we’d ought to keep it that way.

It doesn’t appear to actually be used, at least in Australia, but having the functionality built in at all should be straight up illegal in a caring society.

(/s)

You’re THE object oriented programming?! I’m always asked questions about you. I’m downright starstruck!

I don’t think any of the major (I know someone will probably come in here and tell me about some tiny provider that’s only in like 2 states that does) US carriers that do phones on secured credit, they default to unsecured credit. Maybe, they have an alternative plan for people with not so great credit, but I doubt it.

Someone in the original thread said this swindle does not apply to the US. Though I’m a bit surprised… it’s the first place where I would expect this to happen.

The US carriers install their own software loads onto phones they sell, with similar functionality, they don’t need to use this mechanism.